Can you settle a car accident privately? Yes, you can settle a car accident privately, which means resolving the issue and agreeing on compensation with the other driver without involving insurance companies or the courts. This guide provides a detailed, step-by-step approach to achieving a successful private car accident settlement. This is also known as resolving a car accident without insurance.

Image Source: b2404211.smushcdn.com

Why Consider a Private Car Accident Settlement?

Several reasons might make a private car accident settlement an attractive option:

- Avoid Increased Insurance Premiums: Filing a claim can raise your insurance rates, even if you weren’t at fault.

- Maintain a Clean Driving Record: Some minor accidents might not need to go on your record.

- Faster Resolution: Settling privately can be quicker than dealing with insurance companies, which can be slow and bureaucratic.

- Flexibility: You have more control over the settlement terms and can negotiate directly with the other party.

- Minor Damages: When damages are relatively low, a private car accident damages settlement privately might be the most efficient route.

However, consider these factors before deciding to settle privately:

- Severity of Damages: Private settlements are generally best for minor accidents with clear liability and limited injuries.

- Trust and Cooperation: It requires a good faith effort and open communication from both parties.

- Legal Advice: Even in private settlements, it’s wise to consult with an attorney, especially if injuries are involved.

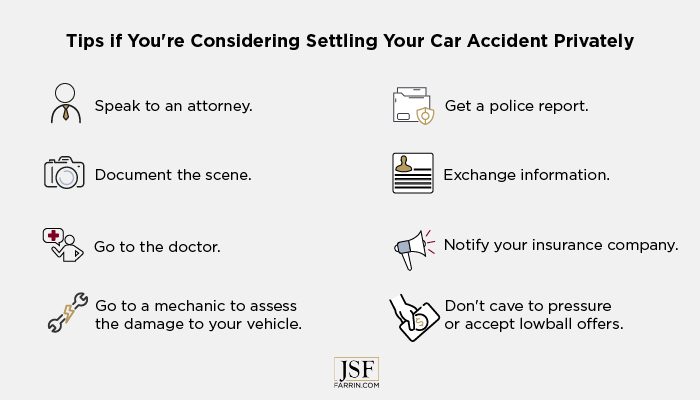

Step 1: Assess the Situation Immediately After the Accident

The actions taken immediately after a car accident are crucial, whether you plan to settle privately or go through insurance.

- Ensure Safety: Check for injuries and move vehicles to a safe location if possible.

- Call the Police: In many jurisdictions, you must call the police if there are injuries or significant property damage. Even if you plan to settle privately, a police report can provide documentation and objectivity.

- Exchange Information: Obtain the following information from the other driver:

- Full Name

- Address

- Phone Number

- Driver’s License Number

- Insurance Company and Policy Number (even if you don’t plan to use it)

- Vehicle Information (Make, Model, Year, License Plate Number)

- Document the Scene: Take photos and videos of:

- Vehicle Damage (both vehicles)

- Accident Scene (road conditions, traffic signals, etc.)

- Injuries (if any)

- Gather Witness Information: If there were witnesses, get their names and contact information.

- Don’t Admit Fault: Avoid saying anything that could be construed as admitting fault. Stick to the facts.

Step 2: Determine Fault and Liability

Figuring out who is at fault is essential for a private car accident settlement.

- Review the Police Report (if available): The police report often includes a preliminary determination of fault.

- Analyze the Evidence: Carefully review photos, videos, witness statements, and the drivers’ accounts.

- Consider Traffic Laws: Understand the traffic laws that apply to the accident. Who had the right-of-way? Did anyone violate traffic signals?

- Comparative Negligence: Some states follow comparative negligence rules, meaning that even if you’re partially at fault, you can still recover damages, but your recovery is reduced by your percentage of fault. This affects negotiating car accident settlement amounts.

Example: If you are found to be 20% at fault for the accident, you can only recover 80% of your damages from the other driver.

Step 3: Assess the Damages

Accurately assessing the damages is critical for a fair car accident damages settlement privately.

- Vehicle Damage:

- Get Estimates: Obtain at least two repair estimates from reputable auto body shops.

- Total Loss: If the cost to repair the vehicle exceeds its market value, it may be considered a total loss. Determine the fair market value of your vehicle before the accident using resources like Kelley Blue Book or Edmunds.

- Medical Expenses:

- Document all Medical Bills: Include doctor visits, hospital stays, physical therapy, medication, and any other medical treatment.

- Future Medical Expenses: If you anticipate future medical treatment, get a written estimate from your doctor.

- Lost Wages:

- Calculate Lost Income: Determine the amount of income you lost due to the accident.

- Documentation: Obtain pay stubs, tax returns, or a letter from your employer to verify your lost wages.

- Pain and Suffering: This is more subjective and difficult to quantify. Factors to consider include the severity of your injuries, the duration of pain, and the impact on your daily life. A common method is the “multiplier” method, where you multiply your medical expenses by a factor (usually between 1.5 and 5) to arrive at a pain and suffering amount.

- Other Expenses: Document any other expenses related to the accident, such as rental car costs, towing fees, or property damage.

Step 4: Contact the Other Driver (or Their Attorney)

Initiate communication with the other driver or their attorney to discuss a private settlement for vehicle accident.

- Polite and Professional: Maintain a respectful and professional tone, even if you disagree.

- Clear Communication: Clearly explain the accident, your assessment of fault, and the damages you have incurred.

- Present Your Evidence: Share your photos, videos, repair estimates, medical bills, and other documentation.

- Listen to Their Perspective: Be open to hearing the other driver’s perspective and understanding their assessment of the situation.

Step 5: Negotiate a Settlement Amount

Negotiation is key to a successful negotiating car accident settlement. This is when your research and preparation pay off.

- Start with a Demand: Begin by making a settlement demand that includes all your damages, including vehicle repair costs, medical expenses, lost wages, pain and suffering, and other expenses.

- Be Prepared to Negotiate: The other driver will likely make a counteroffer. Be prepared to justify your demand and negotiate a fair settlement amount.

- Document All Communication: Keep a written record of all conversations, emails, and letters.

- Compromise: Be willing to compromise to reach an agreement. Consider factors such as the strength of your case, the cost of litigation, and the potential for a higher recovery at trial.

- Negotiation Strategies:

- Anchor: Make the first offer (your demand) to set the tone for negotiations.

- Good Cop/Bad Cop: This involves one person being agreeable and understanding (“good cop”), while the other is firm and demanding (“bad cop”). (Can be a team effort if you are working with someone)

- Limited Authority: Claiming you have limited authority and need to get approval from someone else.

- Walk Away: Be prepared to walk away from the negotiation if you can’t reach a fair agreement.

Step 6: Draft a Car Accident Private Agreement

Once you’ve agreed on a settlement amount, create a written car accident private agreement. This is also known as a car accident private agreement.

- Essential Elements: The agreement should include the following:

- Date of the Accident: The specific date, time, and location of the accident.

- Parties Involved: The full names, addresses, and contact information of all parties involved.

- Description of the Accident: A brief description of how the accident occurred.

- Settlement Amount: The agreed-upon settlement amount.

- Release of Liability: A statement that the settlement is a full and final release of all claims arising from the accident. This prevents the other driver from suing you later.

- Payment Terms: How and when the settlement amount will be paid.

- Governing Law: The state law that will govern the agreement.

- Signatures: Signatures of all parties involved, dated and witnessed (preferably notarized).

Here is a sample clause for the Release of Liability:

In consideration of the payment of $[Settlement Amount] by [Releasing Party] to [Released Party], [Released Party] hereby fully and forever releases, acquits, and discharges [Releasing Party], its agents, servants, employees, officers, directors, successors, and assigns, from any and all claims, demands, actions, causes of action, damages, costs, expenses, and compensation, on account of, or in any way growing out of, the car accident that occurred on [Date of Accident] at or near [Location of Accident]. This release includes, but is not limited to, all claims for personal injuries, property damage, lost wages, medical expenses, pain and suffering, and any other losses or damages, whether known or unknown, suspected or unsuspected, that [Released Party] may have or may hereafter acquire as a result of the car accident.

- Consult an Attorney: It is highly recommended that you have an attorney review the agreement before you sign it to ensure that it protects your interests.

Step 7: Execute the Agreement and Exchange Payment

After everyone agrees to the terms, you should sign and notarize the agreement.

- Signatures: All parties should sign and date the agreement.

- Notarization: Notarizing the agreement adds an extra layer of legal protection.

- Payment: The releasing party should make payment according to the terms of the agreement.

- Proof of Payment: The released party should provide proof of payment, such as a cancelled check or a receipt.

Step 8: Monitor the Situation

Even after settling the case privately, it is important to monitor the situation.

- Ensure the Other Driver Complies: Make sure the other driver adheres to the terms of the settlement agreement, particularly regarding payment.

- Keep Records: Keep a copy of the settlement agreement, proof of payment, and all other relevant documents in a safe place.

- Address Potential Issues: If any issues arise after the settlement, such as unexpected medical complications or further damage to your vehicle, contact the other driver or their attorney immediately.

Risks of Settling a Car Accident Privately

While a private settlement can be beneficial, it also comes with risks:

- Underestimating Damages: You might underestimate the full extent of your damages, especially medical expenses.

- Difficulty Enforcing the Agreement: If the other driver fails to pay, you may have to sue them to enforce the agreement.

- Future Legal Issues: If you release all claims, you cannot pursue further compensation if you later discover more severe injuries or damages.

- The Other Driver Doesn’t Pay: This is a big risk. Always consider how to ensure payment. Escrow services can hold the settlement funds until the agreement is finalized.

- Statute of Limitations: Be mindful of the statute of limitations for car accident claims in your state. If you don’t settle or file a lawsuit before the statute of limitations expires, you lose your right to recover damages.

When Not To Settle Privately

There are situations where settling privately is not advisable:

- Serious Injuries: If you or anyone else involved sustained serious injuries, you should contact an attorney and file a claim with the insurance companies.

- Unclear Liability: If fault is not clear, or if there are conflicting accounts of the accident, it’s best to involve the insurance companies to investigate.

- Significant Property Damage: If the property damage is significant, it’s best to have insurance adjusters assess the damages.

- Uncooperative Driver: If the other driver is uncooperative, unwilling to provide information, or denies responsibility, you should file a claim with their insurance company.

- Hit and Run: If the other driver left the scene of the accident, you should report the accident to the police and file a claim with your own insurance company.

Alternatives to Private Settlement

If a private settlement isn’t feasible, consider these alternatives:

- Mediation: Mediation involves a neutral third party who helps facilitate settlement negotiations between the parties.

- Arbitration: Arbitration involves a neutral third party who hears evidence and makes a binding decision on the claim.

- Small Claims Court: If the damages are relatively low, you can file a lawsuit in small claims court.

- Formal Lawsuit: If the damages are significant, you may need to file a formal lawsuit in civil court.

Grasping Informal Car Accident Settlement

An informal car accident settlement is another name for settling privately. It emphasizes the lack of formal legal processes and the reliance on direct negotiation and agreement between the involved parties. This approach favors simplicity and speed but requires both parties to act fairly and transparently.

DIY Car Accident Settlement: Is It Right for You?

A DIY car accident settlement is when you handle the entire settlement process yourself, from assessing damages to negotiating and drafting the settlement agreement. This approach can save you money on attorney fees, but it requires you to have a solid understanding of the legal issues involved and be prepared to handle the process yourself. It is best suited for accidents with minor damages and clear liability.

Fathoming Settling Accident Claims Privately

Settling accident claims privately is a choice. It allows you more control, faster results, and possibly savings. But do your research and know when it’s best to call the professionals.

Tips for a Successful Private Settlement

- Be Organized: Keep all documents organized and easily accessible.

- Be Patient: The negotiation process can take time. Be patient and persistent.

- Be Reasonable: Be willing to compromise and reach a fair agreement.

- Be Professional: Maintain a respectful and professional tone throughout the process.

- Get Legal Advice: Consult with an attorney to ensure your rights are protected.

FAQ About Private Car Accident Settlements

Q: What if the other driver refuses to pay after signing the agreement?

A: You can sue the other driver to enforce the settlement agreement.

Q: Should I still report the accident to my insurance company if I plan to settle privately?

A: It depends on your insurance policy. Some policies require you to report all accidents, regardless of fault or whether you plan to file a claim. It’s best to check your policy or contact your insurance company for clarification.

Q: What happens if the other driver doesn’t have insurance?

A: If the other driver doesn’t have insurance, you can still try to settle privately, but it may be more difficult to recover damages. You may need to file a lawsuit to obtain a judgment and then attempt to collect from the driver’s assets. You may also have uninsured motorist coverage under your own insurance policy.

Q: Can I include future medical expenses in the settlement agreement?

A: Yes, you can include future medical expenses in the settlement agreement, but you will need to provide documentation from your doctor estimating the cost of future treatment.

Q: What is a release of liability, and why is it important?

A: A release of liability is a legal document that releases the other driver from any further claims arising from the accident. It is important because it prevents the other driver from suing you later.

Q: How long do I have to settle a car accident claim privately?

A: You must settle or file a lawsuit before the statute of limitations expires. The statute of limitations varies by state, so it’s important to check the law in your jurisdiction.

By following these steps and considerations, you can increase your chances of a successful DIY car accident settlement, saving time, money, and potential headaches. Remember that every accident is unique, and consulting with an attorney is always recommended.

Hi, I’m Luigi Smith, the voice behind carrepairmag.com. As a passionate car enthusiast with years of hands-on experience in repairing and maintaining vehicles, I created this platform to share my knowledge and expertise. My goal is to empower car owners with practical advice, tips, and step-by-step guides to keep their vehicles running smoothly. Whether you’re a seasoned mechanic or a beginner looking to learn, carrepairmag.com is your go-to source for all things car repair!